Your company is selling software and a customer in the U.S. is asking you for form W-8BEN-E? You should supply it or risk having 30% of your payment withheld. Some customers might also not place an order at all before receiving this form.

Disclaimer: This blog post is presented for educational and entertainment purposes only. I originally wrote the instructions below for my own company. They might be incomplete, wrong or not applicable to your situation.

Preliminary considerations

- What are software licenses (in tax treaty terms)? For this article, I’m assuming they fall under royalties / copyright.

- Does your country have a tax treaty with the U.S.? How much will you save by filling out from W-8BEN-E? Download table 1 (tax rates…) from this IRS page, find your country and look up the royalties / copyright tax rate:

Points at Malta: Ha-ha!

Official information

- IRS page with form W-8BEN-E, official instructions and further information (download the form and the instructions here).

Other links you might find useful

- Blog post: Form W-8BEN-E for UK limited companies

- Forum: South African Association of Game Makers discussion of form W-8BEN-E

- Key Points about the New W-8BEN-E Instructions from COKALA Tax Information Reporting Solutions (PDF, 2014)

- U.S. business taxes information from Stripe Atlas (in case you’re considering establishing a company in the U.S. just so you won’t have to deal with form W-8BEN-E anymore).

- You could also work with a reseller based in the U.S. to get around this issue. We normally work with FastSpring. Their W-9 form can be found here (PDF).

- Filled out forms from other companies I found on the internet: Avangate (Netherlands), Cleverbridge (Germany), Paddle (UK), Emailtopia (Canada)

Instructions for filling out form W-8BEN-E

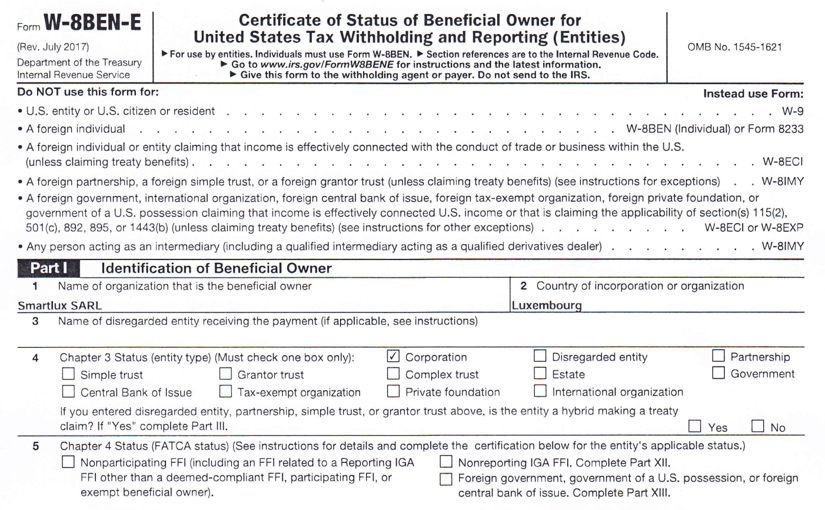

Part I – Identification of Beneficial Owner

Complete line 1 and 2

Check “Corporation” on line 4 (if you’re not working for a corporation, you’re probably reading the wrong blog post).

Skip line 5 (FATCA status) entirely. Software licenses are excluded from the FATCA definition of “withholdable payment” [see: Experis – Finance FATCA Checklist for Multinational Companies (PDF); EY – Information reporting and withholding: the impact of Foreign Account Tax Compliance Act (FATCA) on multinational organizations (PDF)].

Enter address on line 6.

Provide a US taxpayer identification number (TIN) in the form of an employer identification number (EIN) on line 8 or the tax ID assigned in your country on line 9b.

Part III – Claim of Tax Treaty Benefits

Line 14a: Check the box and enter your country.

Line 14b: Check the box at the beginning. Will you have to check another box below? The official instructions say:

If you are a resident of a foreign country that has entered into an income tax treaty with the United States that contains a limitation on benefits (LOB) article, you must complete one of the checkboxes in line 14b. You may only check a box if the limitation on benefits article in that treaty includes a provision that corresponds to the checkbox on which you are relying to claim treaty benefits. A particular treaty might not include every type of test for which a checkbox is provided.

To find out if your country’s tax treaty includes a LOB article (it most probably does), go to the IRS tax treaties tables page and look up your country in table 4 (limitation on benefits). You can find the complete text of the tax treaty through this page and read the articles mentioned in table 4. The official instructions for form W-8BEN-E also contain summarized versions of the LOB tests which might be useful. You should then be able to figure out which box to check.

Line 15: As far as I understood the instructions, this line has to be filled out only “if the treaty contains different withholding rates for different types of royalties.”[see IRS instructions]. Remember table 1 from the very beginning of this blog post? Look at it again. Are all royalties rates the same? If yes, skip line 15, otherwise, fill it in. As “n/a” is not a rate (I hope), I skipped this line (all rates were the same for Luxembourg).

Part XXX – Certification

Sign, fill in print name and date in U.S. format, check the box at the bottom.

Even though I really don’t want to deal with this topic again, I’ll leave the comments open so that you can correct me on all that’s wrong with my instructions. However, please don’t ask me to help you fill out form W-8BEN-E for your company!